If things go according to plan, and the intoxicating hemp market rightfully gets pushed over a cliff later this year, hemp could be stripped down to the nubbins, in a reset back to its original promise for food and fiber.

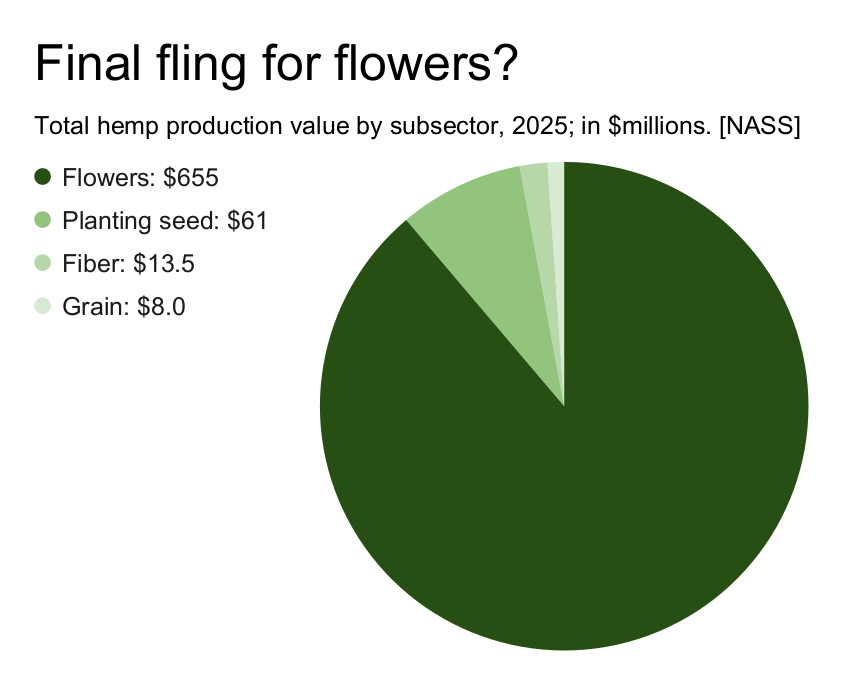

With a combined value of just over $21 million, according to the U.S. Department of Agriculture’s (USDA) annual report on hemp, that “true hemp” core remains minuscule compared to the $655 million estimated for flower production that is likely to get hit hard if a ban on intoxicating hemp takes effect in December, as scheduled.

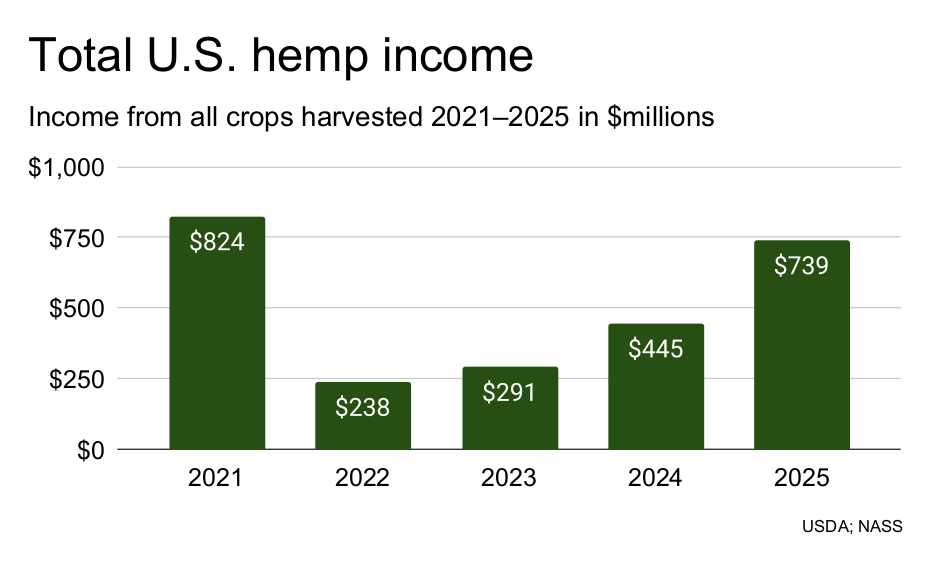

USDA reported total value of $739 million for last year from greenhouse and indoor cultivation, the vast majority of it still tied to flower production.

The USDA/NASS figures should be read as directional rather than definitive. The survey captures farmgate production but excludes downstream processing, imports and finished goods, while also suppressing some state-level data for confidentiality. Despite those limitations, the government report remains the most consistent baseline for tracking the U.S. hemp sector, offering the only nationwide snapshot of production at the farm level.

Fiber imbalance

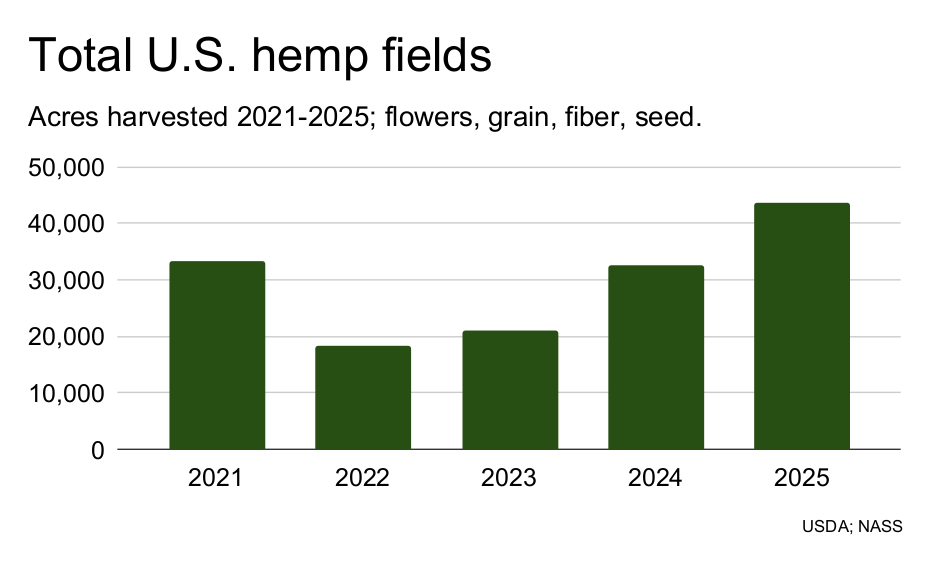

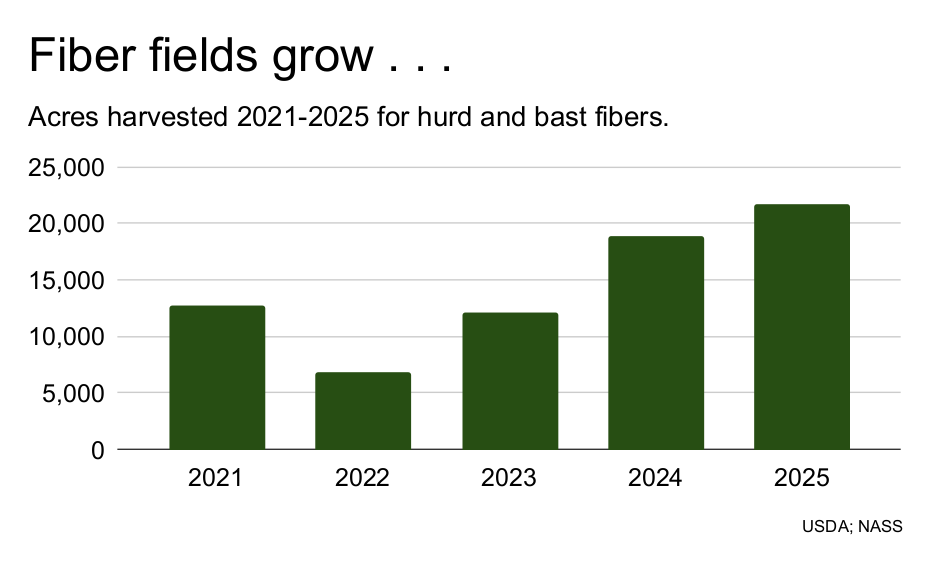

The report, released yesterday by USDA’s National Agricultural Statistics Service (NASS), showed that acreage of stalks grown for hemp hurd and bast fiber for textiles expanded again in 2025.

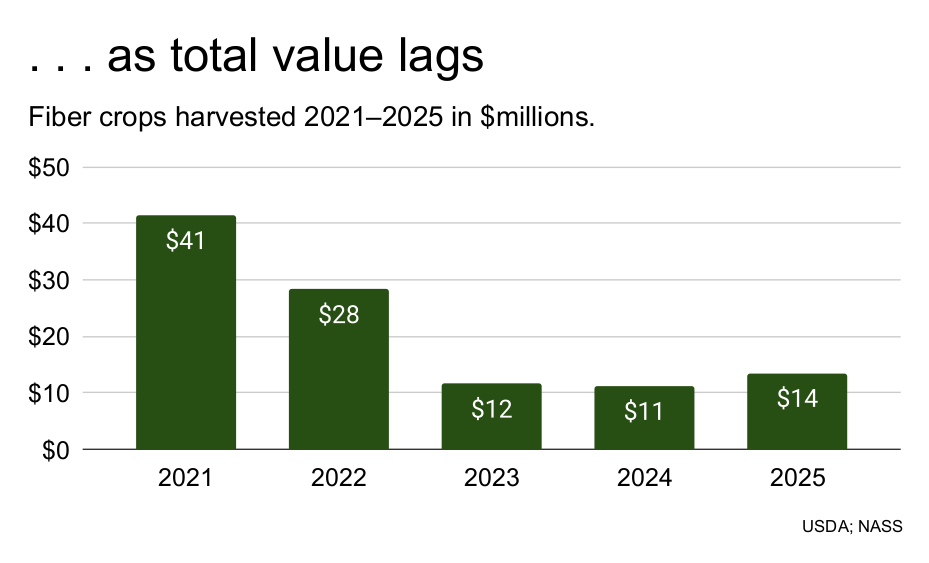

Total fiber value rose from $11.2 million in 2024 to $13.5 million last year. But fiber prices collapsed sharply after 2021 and remain near multi-year lows despite rising output. That means growers had to produce more just to generate the modest increase in revenue. Output is rising, but prices have yet to recover—pointing to a persistent imbalance in the market.

While there is ongoing discussion about demand from Asia, particularly for textile-grade fiber, there are not yet strong indicators that demand has translated into reliable offtake from U.S. producers.

Grain gets noticed

The NASS report showed that the value of grain production reached $8.09 million last year, a jump of 209% year-on-year, while acreage rose 55% nationally in 2025, to 7,515.

While the smaller of the two “true hemp” sectors at the farming level, grain has a clearly defined downstream market in the U.S., with the total for hemp hearts, protein and related products estimated anywhere from $400 million to $700 million. With that demand currently served largely by Canadian imports, U.S. producers appear to be testing the category more deliberately.

Seed multiplication

In a clear indicator that stalwart stakeholders still see a future, production of planting seed was up 190 percent from 2024, with area harvested estimated at 3,537 acres, a jump of 64 percent; the average yield for 2025 was estimated at 573 pounds per acre, up 250 pounds from last year. The value of hemp grown for seed totaled $61 million, making the subsector the biggest behind flowers for CBD.

CBD on a cliff

All of this sits beneath a cannabinoid sector that still dominates the industry’s economics but appears increasingly unstable. In 2025, flowers accounted for roughly 64% of the increase in total hemp value, while driving about 46% of total acreage growth. Those gains, however, are tied largely to intoxicating products derived from CBD — a loophole market that has distorted pricing, supply chains and planting decisions.

A second recent wave of global oversupply has already pushed CBD prices lower, with inventories building across major producing regions. Remove the intoxicating segment, and what remains after that correction is uncertain.

Aside from CBD going into intoxicating hemp products, the original CBD wellness market is not going away, but is difficult to isolate because the out-of-control intoxicant sector has blurred category boundaries and pricing signals.